Introduction

Some members of the PoolTogether community expressed interest in the Olympus DAO Bond program (see @rvdeeb post here). Additionally, Olympus DAO recently launched one of the most successful prize pools on the protocol 3,3Together (already over $20 million deposited and 1,000 users in the first 7 days). Finally, our current LP rewards are scheduled to end in 14 days.

Given the growing synergies between our communities and the popularity of their Bond program. I reached out for more details and jointly wrote up this proposal with Tex who is on their team.

Proposal Overview

This proposal outlines a program for PoolTogether to own its liquidity on AMMs. At the time this proposal is written, there is approximately $1.5M in liquidity for POOL/ETH on Uni V2 ($1.35M) and Sushi ($150k). PoolTogether began incentivizing its liquidity earlier this year at 500 POOL per day and currently has tapered emissions to 300 POOL per day. This is inline with an overall push to lower total emissions and use them more effectively.

Motivation

Implementing bonds reduces the need for POOL incentives over time, which only create temporary liquidity and persistent sell pressure. Importantly, bonds incentivize active PoolTogether community members to participate in the program and help distribute tokens to these users similar to traditional liquidity mining programs.

To make it very basic:

- Currently PoolTogether provides 300 POOL per day in LP incentives. This is “renting liquidity” because as soon as the incentives disappear, the LP’s leave. Leaving nothing behind (this happened when incentives decreased from 500 to 300).

- With a bond program PoolTogether can provide a similar amount of POOL per day to people who GIVE their LP tokens to the protocol permanently. This builds long term value and opens a path to reduce LP rewards to zero.

Specification

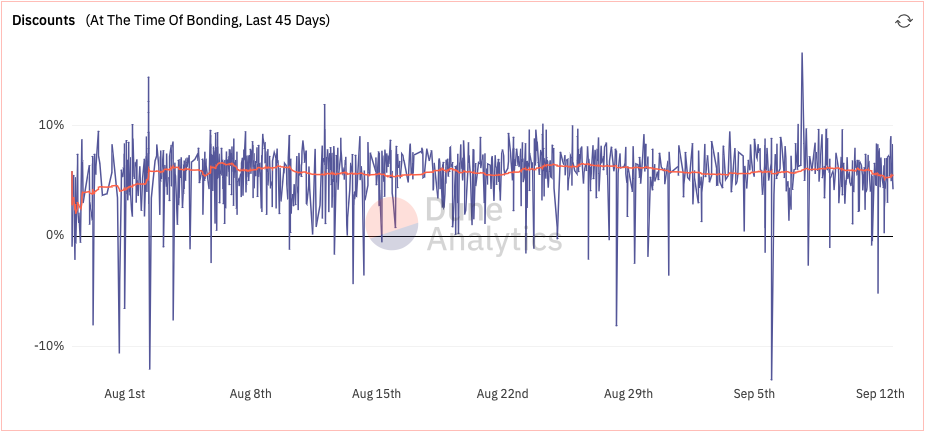

For those unfamiliar with the Olympus bond mechanism, the bond contract essentially sells a token (ex: POOL) at a discount in exchange for assets (ex: POOL/ETH LP tokens). Bonds operate by initializing the price for LP tokens above market price and then applying a discount function that decrements price until a bond is purchased, which pushes the bond price back up. This mechanism allows the market to determine the optimal price for bonds. For reference, here is the average discount of OHM bonds with their extremely high APY:

Olympus is offering to provide its expertise in bond contract management to support other DAOs interested in owning their own liquidity. This will include providing the UI for bonds and maintaining bond control variables to balance emissions with liquidity accumulation. In exchange for the implementation and community engagement, Olympus would take 3.3% of all POOL sold to back OHM tokens. This will align the success of our communities and allow for cross-DAO governance participation.

PoolTogether’s bonds would have a 7-day vesting period to ensure that discount buyers don’t immediately sell into the market. This helps align the goals of bond participants with the goals of the protocol. In addition to purchasing POOL at a discount, bonders know that they are providing permanent liquidity to PoolTogether’s treasury. An additional benefit of bond programs is that they eliminate impermanent loss inherent in traditional liquidity mining and the discount is locked in at the point of purchase.

Proposed Bond Program:

- Accumulate POOL/ETH liquidity

- Bond 14k-20k POOL over 4 weeks

- Vesting period: 7 days

Pros

- Gets a far higher ROI for POOL than we are now

- Helps build a relationship / increased exposure with another large DeFi protocol

- Builds protocol owned POOL/ETH liquidity

- Allows current liquidity incentives to be tapered/eliminated over time

- Lower POOL emissions should improve tokenomics in the long-term

Cons

- Added POOL emissions via bonds may cause sell pressure in the short-term

- 3.3% fee to Olympus Protocol for facilitating the program

- Support using Olympus Pro Bond Program

- Oppose using Olympus Pro Bond Program

0 voters